For most Indian investors, portfolio design has historically been a simple exercise in balance: equity for growth, debt for stability, and gold as a hedge. That trade served well when yields were higher, credit risk was seen as manageable, and equity cycles tended to reward long-term investors with relatively predictable bull phases.

Today, that framework is showing cracks. Global institutional flows are shifting into more sophisticated alternative strategies; fixed-income yields have settled at lower levels than a decade ago; and volatility — punctuated by geopolitical shocks and rapid policy shifts — is more persistent than episodic. In this context, absolute return funds (ARS) emerge not as a novelty but as a structural necessity for modern portfolios.

Let us consider why ARS should be treated as a distinct allocation, how they improve compounding and risk-adjusted returns, and practical steps investors can take to integrate them sensibly.

A maturing global and domestic backdrop

At an industry level, capital flowing to hedge funds and absolute-return strategies has been rising global hedge fund assets reached roughly USD 4.1 trillion in 2024 and industry forecasts point to further growth toward USD 5.5–6.3 trillion by 2030 https://www.marketsmedia.com/hedge-fund-assets-to-reach-5-5-trillion-b — a clear sign of institutional confidence in strategies that target absolute returns rather than benchmark-relative success.

Domestically, India’s alternatives market is maturing AIFs and PMS structures are more commonplace, and after the froth and subsequent normalization of FY24–FY25, long-only AIFs still delivered mid-single-digit to high-single-digit returns in FY25, showing the shifting return dynamics across categories. https://pmsbazaar.com/Blogs/From-Highs-to-Headwinds-How-AIFs-Performed-in-FY2025. This evolution creates the institutional plumbing for absolute return strategies to scale in India. The question for investors is no longer whether such strategies exist — it is whether their portfolio architecture has made room for them.

Meanwhile, the risk-free and benchmark yields investors once relied upon look very different today. The 10-year sovereign yield in India has been hovering around the mid-6% area (recent trading in November 2025 shows yields ~6.5%), a far cry from the high-yield days when core fixed income could deliver meaningful real returns without taking on material credit risk https://in.investing.com/rates-bonds/india-10-year-bond-yield-historical-data Lower yields change the arithmetic of asset allocation: investors who want higher portfolio CAGRs must either take concentrated equity risk or adopt smarter, diversified strategies that sit between debt and equity.

Exhibit 1 – Risk-free yields have fallen — 10-year G-Sec (2015–2025) https://in.investing.com/rates-bonds/india-10-year-bond-yield

What absolute return funds actually deliver

At their essence, absolute return funds seek to generate positive returns across market cycles by using a toolkit that may include long/short equity, arbitrage, options overlays, multi-asset tactical positions, and hedges — the objective being consistent, risk-adjusted alpha rather than outperformance of an index. They are not homogeneous; the strategy mix can vary widely. But the shared promise is steadier compounding and meaningful downside control.

Critically, these funds offer three interlinked benefits for long-term investors:

- Smoother compounding — Instead of relying on a handful of strong equity years to generate lifetime returns, ARS can deliver steady incremental returns through varied market regimes, helping the portfolio compound more reliably.

- An attractive risk-return midpoint — ARS typically presents volatility materially higher than cash/fixed-income but significantly lower than equities, delivering an attractive middle ground for return-enhancement without full equity swings.

- Capital preservation focus — Many ARS prioritize downside management through hedges or market-neutral positioning, which becomes invaluable in range-bound or volatile times.

These are not theoretical benefits — they are measurable outcomes that show up in drawdown statistics, rolling return consistency, and Sharpe ratios over multi-year horizons.

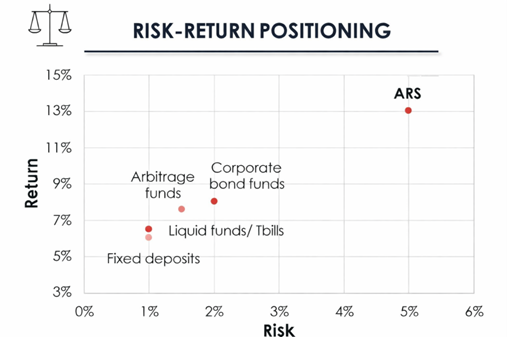

A pragmatic comparison

To see where absolute return funds sit in the investor’s toolbox, the following quick comparisons are useful:

Exhibit 2 – Risk-return equation

Exhibit 3 – Key distinction of ARS compared with other investment approaches

| ARS vs. other investment approaches | Key Distinction |

| Traditional Fixed Income | ARS targets higher returns with market-linked (recoverable) volatility vs. credit-linked (permanent) risk; potential 1.5–2x gross return |

| Credit Strategies | Credit risk is binary and can cause permanent impairment; ARS market risk is temporary and manageable |

| Arbitrage / Liquid Funds | ARS are not parking products — require 12+ month horizon to let strategies play out |

| Balanced Advantage Funds | BAFs carry equity-proximate risk for tax efficiency; ARS offers a genuinely lower-volatility mid-path |

The risk trade-off — market volatility vs credit fragility

One distinction deserves emphasis: credit risk and market risk are not equivalent. A credit event can cause permanent, protracted loss with liquidity disappearing precisely when it is needed most; market volatility, by contrast, is typically temporary and manageable within a disciplined risk framework.

Why timing and horizon matter

Like any strategy with genuine alpha potential, absolute return funds reward patience. A 12–24 month horizon allows the embedded equity-linked and tactical ideas to work through market cycles and demonstrate their edge.

How much allocation makes sense?

Here is a pragmatic, phased approach to integration:

| Phase | Allocation to Fixed Income Sleeve | Move to the Next Phase When… |

| Phase 1 – Experiment (Year 1) | 8–10% | Max drawdown stays within expected band; liquidity terms experienced firsthand |

| Phase 2 – Scale (Years 2–3) | 15–20% | Strategy has performed across at least one volatile and one benign market phase |

| Phase 3 – Normalize (Long-term) | 30–50% | Investor is comfortable with monthly NAV movement and has an established return history |

This framework is most relevant for investors with a fixed-income-heavy portfolio seeking to improve long-run CAGR without materially increasing equity exposure.

Regime evidence and why now is logical

The last few years have shown that volatility regimes can be persistent: sudden geopolitical episodes, policy shifts, and cross-border liquidity movements have produced spikes in market fear gauges. Indian markets are no exception — India VIX has demonstrated substantial episodic spikes in recent years, underscoring that volatility cannot be assumed to be temporary or trivial https://economictimes.indiatimes.com/markets/stocks/news/operation-sindoor-impact-fear-indicator-india-vix-surges-10-as-govt-ups-ante-against-pakistan/articleshow/120985370.cms. Investors who rely solely on the hope that equity bull markets will persist at risk being exposed to longer-than-expected dry spells.

Practical due diligence checklist

- Manager track records across multiple market regimes.

- Transparency on instruments, leverage and derivatives usage.

- Liquidity terms and redemption experience during stress.

- Fee structure and post-tax expected returns (tax treatment matters for comparisons).

- Risk controls: max drawdown limits, value-at-risk processes, and stop-loss frameworks.

A permanent, distinct allocation

Absolute return funds are not a trend. They are a structural response to a world of compressed fixed-income yields, persistent volatility, and the investor’s enduring need for reliable compounding. For portfolios still anchored in a binary equity-debt framework, a modest, disciplined allocation to a well-constructed absolute return strategy is not merely an enhancement — it is an overdue correction.

Disclaimer:

This document is for informational and educational purposes only and should not be regarded as an offer to sell or as a solicitation of an offer to buy or sell the securities or other investments mentioned in it. Recipients are advised to conduct their own research and seek professional advice before making any investment decisions. The document is prepared on the basis publicly available information, internally developed data and other sources believed to be reliable. All opinions, figures, charts/graphs, estimates and data included in this document are as on date specified therein or as on date and are subject to change without notice. The views provided herein are general in nature and do not consider risk appetite or investment objective of any particular investor; readers are requested to take independent professional advice before investing. This document is intended for the direct recipients only and should not be circulated without prior consent of Nuvama Asset Management Limited (“NAML”). The document is not directed or intended for distribution to or use by any person or entity who is a citizen or resident of or located in locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary views to local law, regulation or which would subject NAML and its affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not eligible for sale in all jurisdiction or certain categories of investors. Persons in whose possession this document are required to inform themselves of and to observe such restrictions. Nuvama Asset Management Limited (“NAML”), it’s Holding Company, associate concerns or affiliates or any of their respective directors, employees or representatives do not assume any responsibility for, or warrant the accuracy, completeness, adequacy and reliability of such information or any direct, indirect, special, incidental, consequential, punitive or exemplary damages, including lost profits arising in any way from the information contained in this material. Whilst no action has been solicited based upon the information provided herein, due care has been taken to ensure that the facts are accurate, and opinions given are fair and reasonable. NAML is registered with Securities and Exchange Board of India as a Portfolio Manager vide Registration Number INP000007207 and acts as Investment Manager for various AIF schemes with registered office at 801- 804, Wing A, Building No. 3, Inspire BKC, G Block, Bandra Kurla Complex, Bandra East, Mumbai – 400 051. Corporate Identity No: U67190MH2019PLC343440.

0 comments