The Goods and Services Tax (GST), initially introduced in July 2017, was undoubtedly one of the country’s most notable indirect tax reforms. Creating a ‘One Nation, One Tax’ framework, it was brought into effect to simplify taxation, boost transparency and enhance compliance.

But as of 2025, its initial four slab structure (5%, 12%, 18% and 28% with additional cess in certain cases) has undergone an unprecedented change. GST 2.0, approved during the 56th GST Council meeting in early September this year, substitutes the previous structure with a largely two-tier rate structure (5% and 18%).

This has been largely claimed to help reduce prices, drive demand, and facilitate growth. But how exactly will this come to be? We answer this question by discussing what GST 2.0 is and how it impacts consumption in India right here

“GST 2.0: What it is?”

GST 2.0 reduces the four slabs—5%, 12%, 18% and 28% into a mostly two-tier rate structure—5% and 18%, along with a 40% rate on specific items falling under the category of sin or luxury goods. The 12% and 28% GST slabs have been completely scrapped, with key essentials (household items such as toothpaste, soaps and Indian breads) being subject to lower or Nil tax brackets, driving affordability.

This next-gen GST reform, effective from 22nd September 2025, is aimed at improving the life of the common man while driving ease of doing business. Further, it has been described as a festive gift from the government to the country, given its strategic roll-out timeline.

Impact of GST 2.0 Across Avenues

The idea behind GST 2.0 is not just to reduce tax rates, but to kickstart a cycle of growth with increased consumption. Reducing tax on goods and services makes them more affordable, increasing demand and consumption.

For instance, early government estimates suggest that GST 2.0 is expected to reduce average household grocery and essentials bills by nearly 13%, as several daily-use items have moved to lower or nil tax brackets. Staples such as medicines, earlier taxed at 5%, are now fully exempt, while ghee and butter have shifted from the 12% to 5% slab. Similarly, consumers are likely to experience 7–12% savings on stationery, clothing, footwear, and other daily purchases, and as much as 18% on life and health insurance premiums, which have now been fully exempted from GST.

But zoom out, and this consumption also results in a larger tax base, which in turn, drives revenue and increases economic growth.

All this ultimately sets the stage for long-term capacity building that drives the Indian economy towards self-sufficiency. Considering today’s volatile global markets with wars and tariffs, India needs to be prepared to reduce its reliance on foreign trade. GST 2.0, by driving consumption, achieves just that.

From a macro-fiscal standpoint, GST 2.0’s implications extend beyond just consumer prices and spending. The rationalization of tax slabs is expected to have a mildly disinflationary effect in the short term as lower tax incidence translates into reduced retail prices across several goods and services. This should help the RBI maintain its inflation target band without compromising on growth.

On the fiscal positioning front, the reform enhances transparency and tax buoyancy, improving revenue predictability for both the Centre and States. In the medium term, this is likely to strengthen India’s fiscal balance and reinforce investor confidence in the government’s reform-oriented stance.

Viewed through a growth lens, GST 2.0 can catalyze domestic demand-led expansion — a critical cushion amid global uncertainty. By lowering effective prices and boosting purchasing power, it supports a virtuous cycle of consumption, investment, and employment generation.

GST (1) 2.0: Sectors in Focus

The benefits of GST 2.0 are also visible across discretionary spending categories. Air-conditioners have become cheaper by INR 2,800–INR 5,900, and large-screen televisions have seen price reductions ranging from a few thousand rupees at entry levels to nearly INR 85,000 for ultra-premium models. Dishwashers, too, are now more affordable with price cuts of up to INR 8,000.

In the automobile segment, price reductions are particularly significant. Entry-level hatchbacks are now INR 40,000– INR 75,000 cheaper, with the effective tax rate dropping from 29–31% to 18%. Compact SUVs are lower by up to INR 85,000, while mainstream SUVs have seen cuts exceeding INR 1 lakh. Even two-wheelers have benefited — scooters and motorcycles below 350 cc, which form the bulk of India’s commuter market, now attract 18% GST instead of 28%, leading to savings of INR 7,000– INR 18,800 per unit.

GST 2.0 is set to favourably impact some of the key sectors, driving their consumption rates. Here’s a look at these:

- Automobiles

The auto sector benefits significantly from GST 2.0. Vehicles, whether two-wheelers or four-wheelers, small or big, private or commercial, will all become more affordable. Further, with the festive season just around the corner, when GST 2.0 comes into effect, the sector is poised to experience a strong surge in demand.

Lastly, the auto ancillary businesses, such as battery and tyre makers, will also see a fall in GST (from 18% to 5%). That said, luxury vehicles and premium motorcycles (<350 cc) will be taxed at a rate of 40%.

- Consumer Staples and FMCG

Daily essentials such as toothpaste, hair oils, packaged foods and dairy products will benefit from a sharp tax cut (from 18% to 5%), reducing their price and driving purchase volumes and hence consumption. This is believed to especially benefit lower and middle-income groups.

- Building Materials

Real estate and rural construction industries will benefit from GST 2.0, as the GST rate is reduced from 28% to 18%. Further, a reduced GST on slag products and fly-ash bricks will also incentivise sustainability-focused real estate projects.

Considering India’s commercial real estate is set to double by 2029, growing at a CAGR of a whopping 21%, this added support of lower GST can further bolster the industry’s growth.

- Insurance and BFSI

The GST 2.0 also exempts premiums for individual life and health insurance from GST, driving insurance affordability. With a lower insurance premium obligation, individuals are better positioned to apply for and get approvals for credit requests.

This will naturally translate into a higher credit demand for NBFCs and banks, strengthening the BFSI sector simultaneously.

- Hospitality

Under GST 2.0, hotels will be subject to 5% (without ITC) for rooms booked for up to INR 7,500 per night. Above this threshold, the GST remains unchanged at 18% (with ITC).

Further, the Quick Service Restaurant (QSR) sector will also experience a fall in price, and therefore a rise in consumption. This is the result of the reduction in GST (from 18% to 5%) on FMCG products such as cheese, coffee, ice cream, and chocolate.

While the reform broadly benefits the economy, its impact differs across industries.

- Winners: Consumer staples, FMCG, auto, real estate, and hospitality emerge as clear beneficiaries, driven by lower effective tax rates and higher affordability. Insurance and BFSI also gain from enhanced affordability and credit demand.

- Neutrals: IT services, telecom, and pharmaceuticals remain largely unaffected as their existing GST rates are retained.

- Relative Losers: Certain luxury and sin goods — such as premium vehicles, tobacco, alcoholic beverages, and aerated drinks — now attract a higher 40% rate, marginally suppressing their demand but supporting fiscal discipline.

Overall, GST 2.0 appears pro-growth and pro-consumption in orientation, with limited adverse sectoral spillovers.

Will GST 2.0 Benefits Trickle Down to the Consumer?

GST 2.0 can only have its intended effect on consumption levels if the benefits of reduced tax translate into price reductions. To ensure this, the government introduced anti-profiteering rules under GST. Section 171 of the CGST Act, 2017, empowers authorities to monitor, investigate and punish businesses that don’t transfer GST benefits to the end customer.

However, as per the GST Council’s recommendations, no new anti-profiteering complaints have been accepted after 1 April 2025. This has been done to allow market forces to decide pricing. The lack of recourse can naturally sound alarm bells. But the revenue secretary has addressed concerns by reassuring that the industry will ensure tax rate cuts are effectively realized in price reductions.

How Does GST 2.0 Affect State Revenue?

The tax amount reduces substantially under GST 2.0. So, it is logical to conclude that it will also reduce revenue for the state governments.

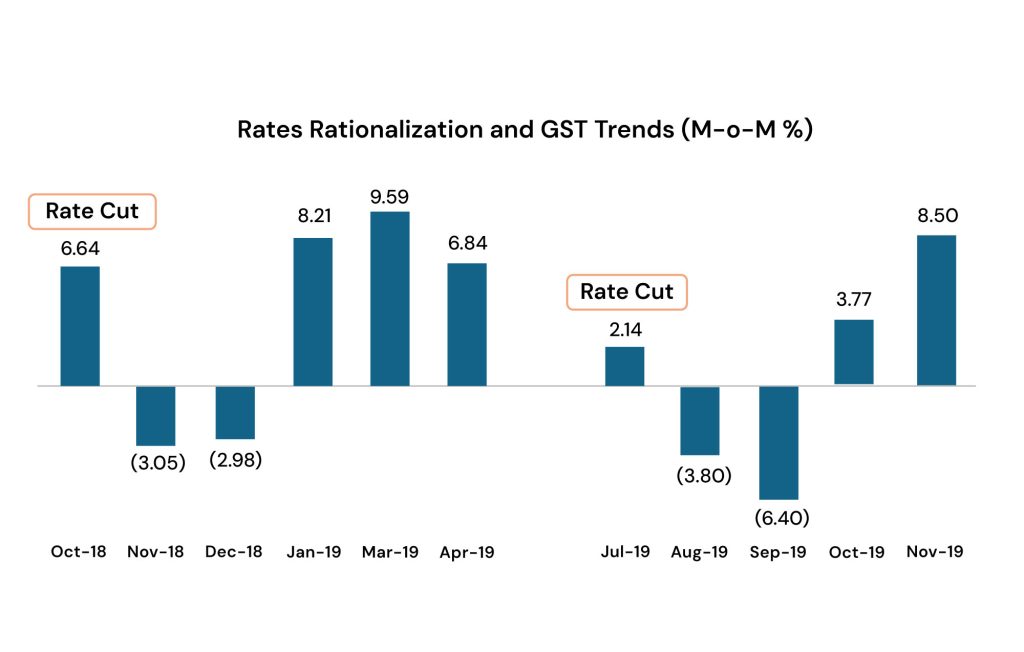

But that is not the case on the ground. In fact, as per State Bank of India’s (SBI) research, every time GST rates have been revised in the past (July 2018 and October 2019), states have witnessed only a temporary adjustment phase followed by stronger revenue inflows. An initial revenue fall of 3-4% is usually followed by a sustained growth of 5-6% per month.

The reason why government treasuries have never and will never pay the price for rate rationalization under the GST regime is the unique revenue-sharing architecture of the tax. You see, GST is split equally between the Centre and the States. But with the tax devolution mechanism, 41% of the Centre’s GST share goes back to the States.

So, let’s say if GST amounting to INR 1000 is collected, states actually receive INR 70.5, nearly 70% of the country’s GST revenues.

Coming back to GST 2.0, SBI says that states are expected to receive a minimum of INR 10 lakh crore in SCGST and INR 4.1 lakh crore through tax devolution in FY26, making them net gainers. And this, mind you, is when we don’t take the additional consumption boost into account. Once that gets factored in, states’ revenue earnings will naturally be higher. All in all, states’ revenue also experiences a positive surge with GST rate rationalization under GST 2.0.

Final Thoughts

GST 2.0 is easily one of the most significant tax reforms undertaken in recent history. By simplifying the GST structure and consequently easing the tax processes, this next-gen GST structure is well-positioned to drive consumption in the country. As a result, paving the way for a more self-reliant Indian economy.

GST 2.0 will prove to be a catalyst for a more stable and thriving economy. Further, this will not be an isolated event either. The Indian Prime Minister has promised that more reforms that safeguard India from global market volatility are to come.

Beyond simplifying the tax framework, GST 2.0 isn’t a one-year tax change — it is a structural move that improves visibility across consumption, corporate margins, formalisation, and fiscal predictability. It:

- Supports India’s domestic growth thesis

- Raises confidence in earnings visibility across sectors

- Bolsters long-term portfolio repositioning by reducing cyclical volatility

- Expands the investable universe in both private and listed markets

From a market strategy perspective, investors can look to “play the GST 2.0 theme” through sectors that directly benefit from consumption growth — autos, FMCG, real estate, and financials. Listed companies in these segments stand to gain from better pricing power, margin expansion, and stronger earnings growth visibility.

For India, the broader benefit lies in how GST 2.0 enhances competitiveness within Asia. With lower indirect tax frictions and improved cost efficiency, India could outperform its Southeast Asian peers as a manufacturing and consumption hub. This reform therefore not only simplifies taxation but also positions India as a more attractive destination for capital, production, and talent in the decade ahead.

References

- https://gstcouncil.gov.in/about-us-archive#:~:text=One%20Nation%2C%20One%20Tax%3AGST,the%20cascading%20effect%20of%20taxes.

- https://www.newindianexpress.com/web-only/2025/Sep/12/gst-20-and-the-mirage-of-consumption-led-growth

- https://www.mymoneysage.in/gst-2-0-a-turning-point-for-indias-consumption-led-growth/

- https://cleartax.in/s/anti-profiteering-gst-law

- https://www.pib.gov.in/PressNoteDetails.aspx?id=155151&NoteId=155151&ModuleId=3

- https://sbi.bank.in/documents/13958/14472/GST+2.0_An+Update_SBI+Research.pdf/5ff28655-c419-4a82-e856-324f6690fdb9?t=1756792109167

- https://economictimes.indiatimes.com/wealth/tax/do-gst-cuts-really-translate-into-genuine-savings-for-buyers/articleshow/124176570.cms?from=mdr

- https://www.thehindu.com/news/national/new-gst-rates-goods-and-services-cheaper-live-updates-september-22-2025/article70079103.ece

Disclaimer:

This document is for informational and educational purposes only and should not be regarded as an offer to sell or as a solicitation of an offer to buy or sell the securities or other investments mentioned in it. Recipients are advised to conduct their own research and seek professional advice before making any investment decisions. The document is prepared on the basis publicly available information, internally developed data and other sources believed to be reliable. All opinions, figures, charts/graphs, estimates and data included in this document are as on date specified therein or as on date and are subject to change without notice. The views provided herein are general in nature and do not consider risk appetite or investment objective of any particular investor; readers are requested to take independent professional advice before investing. This document is intended for the direct recipients only and should not be circulated without prior consent of Nuvama Asset Management Limited (“NAML”). The document is not directed or intended for distribution to or use by any person or entity who is a citizen or resident of or located in locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary views to local law, regulation or which would subject NAML and its affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not eligible for sale in all jurisdiction or certain categories of investors. Persons in whose possession this document are required to inform themselves of and to observe such restrictions. Nuvama Asset Management Limited (“NAML”) , it’s Holding Company, associate concerns or affiliates or any of their respective directors, employees or representatives do not assume any responsibility for, or warrant the accuracy, completeness, adequacy and reliability of such information or any direct, indirect, special, incidental, consequential, punitive or exemplary damages, including lost profits arising in any way from the information contained in this material. Whilst no action has been solicited based upon the information provided herein, due care has been taken to ensure that the facts are accurate, and opinions given are fair and reasonable. NAML is registered with Securities and Exchange Board of India as a Portfolio Manager vide Registration Number INP000007207 and acts as Investment Manager for various AIF schemes with registered office at 801- 804, Wing A, Building No. 3, Inspire BKC, G Block, Bandra Kurla Complex, Bandra East, Mumbai – 400 051. Corporate Identity No: U67190MH2019PLC343440

0 comments