The first half of 2025 has reaffirmed what many investors have begun to recognise: volatility is no longer intermittent, it is structural. While the Nifty has touched record highs, concerns over stretched valuations, shifting global liquidity, and persistent geopolitical tensions have created an undercurrent of uncertainty. Market direction has become harder to predict, and traditional long only portfolios, especially those reliant on equity beta, are finding it increasingly difficult to deliver consistency.

In this environment, absolute return strategies (ARS) offer a compelling alternative. Built to deliver consistent returns independent of market direction, absolute return strategies employ a blend of long, short, and arbitrage positions thereby prioritizing capital preservation and alpha generation through security selection, tactical agility, and disciplined risk management.

ARS are designed to cushion portfolios during uncertain phases — unlike relative return funds, which remain benchmark-bound and can underperform in downturns.

Capital preservation and low volatility at the core

At their heart, absolute return strategies offer a simple promise: preserve capital first, grow it second. Their ability to limit drawdowns and deliver consistent performance is particularly valuable in today’s choppy, range-bound markets, a hallmark of 2025 so far.

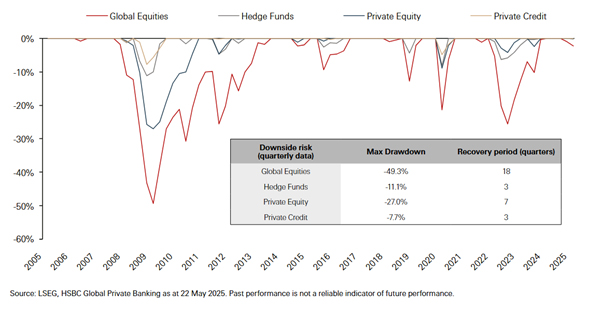

Globally, Hedge funds, which are long-time practitioners of ARS have historically demonstrated resilience, with maximum drawdowns limited to – 11.1%, compared to – 49.3% for global equities, as depicted in Exhibit 1 . Recovery periods have been shorter too, typically under three quarters.

Exhibit 1: Being practitioners of absolute return, Hedge funds have demonstrated better resilience

Today, Global hedge fund assets stand at $4.1 trillion (2024) and are projected to reach $5.5–6.3 trillion by 2030 ,with 15–20% allocated to absolute return and market-neutral strategies , underscoring institutional confidence. In India, the numbers are relatively smaller but compelling.

Inside the toolkit: how Absolute Return strategies navigate uncertain markets

| Strategy | Decoding the concept |

| Long-short strategies: profit on both sides | Popularized by Alfred Winslow Jones, this strategy involves going long on assets expected to rise and short on those likely to fall. It helps reduce exposure to overall market direction—hence the term “market neutral.” While widely used in equities, it’s equally applicable to bonds. |

| Long-only multi-asset: diversify to reduce risk | Built on Harry Markowitz’s principle of diversification, these funds combine low-correlated assets to lower overall portfolio risk. Typically, long-only, they span equities, bonds, and alternatives like infrastructure and private equity—areas retail investors often can’t access directly. |

| Macro funds: the wider lens | Macro strategies take a top-down view, investing based on global economic themes—rates, inflation, policy shifts—rather than company specifics. Managers use futures, options, and currencies to take long or short positions across markets, allowing nimble positioning. |

| Multi-strategy: many bets, one portfolio | These funds blend multiple approaches—arbitrage, relative value, sector spreads, and more—to create uncorrelated return streams. A manager might be simultaneously exploiting mispricing in interest rate futures, trading volatility in equity options, and running a convergence strategy between two currencies. |

Relative vs absolute return: the benchmark bias

Relative return managers are often tied to benchmarks. They may be forced to hold sectors just because they are part of the index—even if those sectors look overvalued. Since indices are backward-looking, they tend to overweight past winners and underweight potential future performers. In India, sectors like IT, financials, or PSUs have seen major index shifts driven by recent momentum and fundamentals.

Think of it like trying to beat a competitor in a race—your focus is always on how they’re performing, not just on running your best.

Absolute return managers, in contrast, aim to deliver positive returns regardless of what the benchmark does. They are not forced to follow index weightings and can avoid sectors with unfavourable risk-reward. Their goal is simple: generate consistent, risk-adjusted returns. That flexibility makes them better equipped to adapt in volatile markets.

Why absolute return strategies matter today

Volatility is here to stay

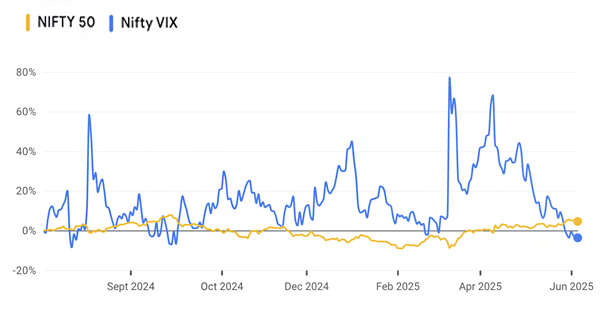

Over the past year, volatility has become a constant. In April 2025, the Nifty VIX spiked 77% as the Nifty 50 fell 9%. In May 2025, a 64% jump in VIX came with just a 1.2% decline, while in August 2024, volatility rose 58% with barely a 1% drop. These patterns make it clear volatility is here to stay, making the case for absolute return strategies stronger than ever.

Exhibit 2: Movement of Nifty VIX and Nifty 50, indicates

- HNIs and family offices are reprioritizing

There’s a clear shift toward capital efficiency and risk-managed alpha. ARS are no longer fringe allocations; they are being embedded at the core of long-term wealth strategies.

- India’s alternatives market is maturing.

With AIFs and PMS now well-established, ARS have room to scale. Investor commitments to AIFs have quadrupled in four years, a surge driven in part by the anticipated 50% increase in the country’s ultra-rich population by 2028. Clearly, the wealthiest investors are betting big on alternatives and absolute return strategies to generate higher returns with diversification and risk control. For investors who’ve fully capitalized on traditional equity and debt, these strategies offer the next frontier of sophistication.

| NARS and NARS+ — built for this moment. At Nuvama, our Nuvama Absolute Return Strategy (NARS) and NARS+ strategies offer investors access to curated, institutional-grade absolute return strategies through both PMS and AIF platforms respectively. These adaptive strategies aim for consistent, risk-adjusted alpha by blending long/short equity, arbitrage, and multi-asset exposures with disciplined risk management. Born from the 2023 budget’s impact on traditional fixed income, NARS is specifically engineered to deliver 9-10% post-tax returns—targeting a 200-300 bps alpha over conventional debt without high volatility. It is structured for superior tax efficiency and robust downside protection, designed to avoid losses even in a 10% market decline. This makes NARS a forward-looking solution, adapted to meet modern investor needs. |

Disclaimer:

Performance related information provided hereunder is not verified by SEBI or any regulatory authority. The performance is based on TWRR. As per SEBI guidelines, returns are net of all expenses and investor returns may differ, based on their period of investment, fee structure and point of capital flows. Please note that performance of your portfolio may vary from that of other investors and that generated by the Investment Approach across all investors because of 1) the timing of inflows and outflows of funds; and 2) differences in the portfolio composition because of restrictions and other constraints. Performance calculated also considers liquid investments and cash. Nuvama Asset Management Limited is registered with Securities and Exchange Board of India as a Portfolio Manager vide Registration Number INP000007207. Securities investments are subject to market risks and there is no assurance or guarantee that the objectives of the Investment Approach will be achieved. Any change in the investment approach may impact the performance of the client’s portfolio. Past performance of the Portfolio Manager/Investment Approach may not be indicative of the performance in the future and no representation or warranty expressed or implied is made regarding future performance. Investors are advised to take independent tax, legal, risk, financial and other professional advice and refer to the Disclosure Document available on the website https://www.nuvama.com/our-businesses/asset-management/ for detailed risk factors/disclaimers. For a detailed disclaimer, please click here. This document is for informational and educational purposes only and should not be regarded as an offer to sell or as a solicitation of an offer to buy or sell the securities or other investments mentioned in it. Recipients are advised to conduct their own research and seek professional advice before making any investment decisions. The document is prepared on the basis publicly available information, internally developed data and other sources believed to be reliable. All opinions, figures, charts/graphs, estimates and data included in this document are as on date specified therein or as on date and are subject to change without notice. The views provided herein are general in nature and do not consider risk appetite or investment objective of any particular investor; readers are requested to take independent professional advice before investing. Document is intended for the direct recipients only and should not be circulated with consent NAML. The document is not directed or intended for distribution to or use by any person or entity who is a citizen or resident of or located in locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary views to local law, regulation or which would subject NAML and its affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not eligible for sale in all jurisdiction or certain categories of investors. Persons in whose possession this document are required to inform themselves of and to observe such restrictions. Nuvama Asset Management Limited (“NAML”), it’s Holding Company, associate concerns or affiliates or any of their respective directors, employees or representatives do not assume any responsibility for, or warrant the accuracy, completeness, adequacy and reliability of such information or any direct, indirect, special, incidental, consequential, punitive or exemplary damages, including lost profits arising in any way from the information contained in this material. Whilst no action has been solicited based upon the information provided herein, due care has been taken to ensure that the facts are accurate, and opinions given are fair and reasonable. NAML is registered with Securities and Exchange Board of India as a Portfolio Manager vide Registration Number INP000007207 and acts as Investment Manage for various AIF schemes with registered office at 801- 804, Wing A, Building No. 3, Inspire BKC, G Block, Bandra Kurla Complex, Bandra East, Mumbai – 400 051. Corporate Identity No: U67190MH2019PLC343440.

0 comments